Application Provision

1

Introduction

1.1

Footnotes

- 1. October 2018: https://www.bankofengland.co.uk/prudential-regulation/publication/pras-approach-to-supervision-of-the-banking-and-insurance-sectors.

- 2. PRA designated investment firms list: http://www.bankofengland.co.uk/prudential-regulation/authorisations/which-firms-does-the-pra-regulate.

- 3. March 2018: https://www.bankofengland.co.uk/prudential-regulation/publication/2018/international-banks-pras-approach-to-branch-authorisation-and-supervision-ss.

- 26/07/2021

1.2

Although this SS largely consolidates the PRA’s existing approach to international banks, the PRA recognises that firms (including firms operating with deemed authorisations under the temporary permissions regime (TPR)) may need additional time to adjust.4 Accordingly, the PRA will adopt a proportionate approach to implementation. Firms operating under the TPR will not need to meet the expectations in this SS immediately, but will need to do so as soon as practicable (taking into account their individual business model and systemic impact), and in any event by the time they are authorised by the PRA and exit the TPR. As part of pre-authorisation discussions, the PRA will expect such firms to demonstrate how they intend to meet these expectations. The PRA expects all other authorised firms within the scope of this SS to meet the expectations set out within a reasonable time, taking into account the firm’s current position and the scale of change that might be required. These firms should provide their supervisors with a clear explanation of any gaps they need to address and their proposed timeframe for doing so.

- 26/07/2021

1.3

Many of the expectations in this SS apply both to subsidiaries and to firms operating through a UK branch. To the extent possible, this SS seeks to draw a distinction between the PRA’s expectations which are specific to UK branches or to UK subsidiaries (rather than those that apply to both). While this SS draws out and elaborates on matters discussed in other SSs that are particularly relevant for international banks, it is to be read with, and does not replace, international banks’ obligations under applicable legislation, the PRA’s rules, and the expectations set out in its policy publications.5

Footnotes

- 5. Available at: https://www.bankofengland.co.uk/prudential-regulation/policy.

- 26/07/2021

1.4

This SS sets out the PRA’s expectations for receiving information concerning the risks in the wider group and co-operation from other supervisory authorities concerned with the firm or its wider group.6 This is necessary for the PRA to be satisfied that the international bank is meeting threshold conditions, particularly the threshold condition concerning the effective supervision of the firm. This SS also sets out expectations of international banks in meeting the threshold condition on the prudent conduct of business, including their systems and controls and risk management.

Footnotes

- 6. In this SS, references to a group include, in the case of a branch, the legal entity of which the branch forms part.

- 26/07/2021

1.5

This SS is structured as follows:

- Chapter 2 summarises the PRA’s overall approach and the relationship between (i) a firm’s size and systemic importance; (ii) the information, co-operation, and controls likely to be required to be effectively supervised; and (iii) the degree of independence between UK and overseas business.

- Chapter 3 then elaborates on the first of those points – the relationship between a firm’s size and systemic importance – as well as setting out some general expectations.

- Chapter 4 expands on the information, co-operation, and controls likely to be required to be effectively supervised.

- Chapter 5 explains how the degree of independence between UK and overseas business in the firm or group needs to be commensurate with the two factors above and, in particular, how the PRA may use its supervisory tools, if necessary, to ensure that this is achieved.

- Chapter 6 explains additional expectations the PRA has for firms operating in the UK through a branch, whether or not they are part of a wider group. In particular, it sets out in more detail the specific factors considered when deciding whether to authorise firms to undertake activities in the UK as a branch or a subsidiary instead.

- 26/07/2021

2

Overall approach of responsible openness

2.1

The PRA’s supervisory approach is grounded in the risks to its statutory objective of promoting the safety and soundness of PRA authorised firms, particularly by seeking to avoid adverse effects on the stability of the financial system of the UK. The PRA has to be satisfied that a firm is capable of meeting threshold conditions on an ongoing basis, including the requirement that it is capable of being effectively supervised by the PRA. For international banks, this will depend in part on the risks in the wider group being visible to the PRA, and the level of co-operation and information it is receiving from the firm and relevant overseas supervisory and resolution authorities.7 This is because the PRA needs to understand what risks the UK branch or subsidiary is exposed to and how these are dependent on the business and risk profile of the rest of the firm or the group.

Footnotes

- 7. ‘Home jurisdiction’ and ‘home state supervisor’ refer to the jurisdiction and supervisory authority that has assumed responsibility for consolidated prudential supervision where a firm is part of a group, together with any other jurisdiction or supervisory authority with a regime that is particularly relevant to the way in which an international bank does business in the UK. They also include the supervisory authority responsible for the prudential supervision of a firm with a UK branch. ‘Home resolution authority’ refers to the resolution authority responsible for the resolution of the overall group and coordination of resolution plans.

- 26/07/2021

2.2

For UK subsidiaries of groups based outside the UK, the PRA applies the same regulatory requirements and follows the same supervisory framework as for firms that are based in the UK and are either not part of a group or are part of a group based in the UK. However, its supervisory approach takes into account the links between the subsidiary and the rest of the group of which it forms a part. Where that group is not based in the UK, the PRA will typically have less information on the risks arising in the group, and less ready access to those responsible for group risk management. The PRA tailors its supervisory approach according to the nature, scale, and complexity of a firm’s UK operations and potential impact on financial stability in the UK, and also according to the extent to which the UK operations are integrated with overseas operations. Accordingly, the PRA’s expectations of subsidiaries of groups based outside the UK may well differ in some areas from those of subsidiaries belonging to groups based in the UK. Details of how the PRA’s expectations vary in this regard are set out in this SS.

- 26/07/2021

2.3

For firms that operate through a UK branch, the branch forms part of a legal entity incorporated outside the UK. It follows that its operations are necessarily dependent on those of the legal entity as a whole. It will be subject to prudential regulation by its home state supervisory authority according to where it is based. Unlike UK subsidiaries, the PRA applies a different set of rules to such firms, recognising that while PRA authorisation applies to the whole firm, it is appropriate to rely on the home state supervisor for certain aspects of supervision. The expectations that the PRA has for information relevant to the PRA’s objectives will therefore also vary in this regard.

- 26/07/2021

2.4

The Financial Conduct Authority (FCA) is the conduct regulator for all banks and investment firms operating in the UK. Therefore, for such firms, whether operating as subsidiaries or through branches in the UK, the FCA’s threshold conditions and conduct of business rules apply, including in areas such as anti-money laundering. Authorisation can be granted only where both the FCA and the PRA are satisfied that their respective requirements have been met. The FCA will independently assess applicants against its own requirements and objectives.

- 26/07/2021

2.5

Subject to these foundations, the PRA recognises the efficiency benefits that banks’ international operations can bring. As such it is open, in principle, to hosting subsidiaries of international groups that operate a highly integrated global business model, and to allowing firms to operate in the UK through a branch or subsidiary.

- 26/07/2021

2.6

The PRA recognises that many wholesale businesses, and investment banking and trading in particular, are operated on a global and highly integrated basis.

- 26/07/2021

2.7

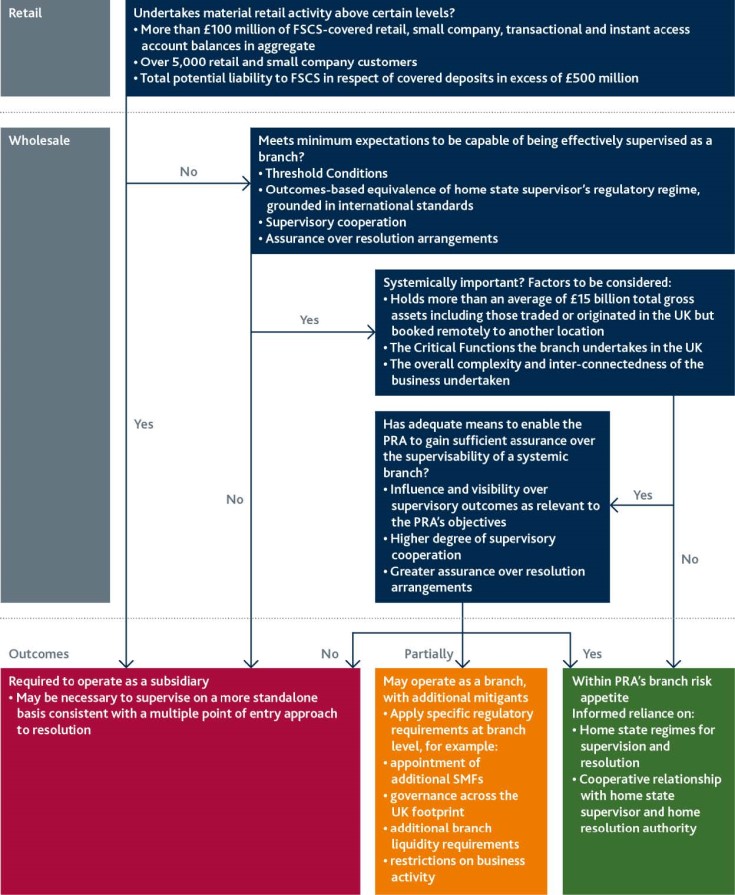

The PRA has different expectations for businesses that engage in retail banking activities, since those activities tend to have a greater effect on financial stability. Additional requirements would apply to firms that would fall within the scope of the UK’s ring-fencing regime.8 Large retail banking activities can be more effectively supervised if they are separated from other activities in the wider group. Above certain thresholds, the PRA will consider authorising firms as subsidiaries in the UK rather than permitting them to operate through a UK branch, thereby increasing the separation of the UK retail business from risks arising overseas.9 However, below the threshold at which ringfencing requirements apply, the PRA does not have any greater expectation for the separation of retail business. It does, however, expect to receive more information on any financial and operational dependencies (including cross-subsidies) between that retail business and wholesale business, whether within the same firm or between related group entities.

Footnotes

- 8. https://www.bankofengland.co.uk/prudential-regulation/key-initiatives/ring-fencing.

- 9. One threshold is £100 million of retail and small company transactional deposits, but the PRA also considers the number of such deposit accounts and the total potential liability to the Financial Services Compensation Scheme. See Chapter 6 for full details.

- 26/07/2021

2.8

- 26/07/2021

2.9

Each element in Figure 1 is considered below in more detail.

- 26/07/2021

2.10

It should be noted, however, that apart from ring-fencing requirements, there is no automatic or fixed outcome that the PRA applies in terms of the degree of integration or separation that is appropriate. The PRA applies a graduated set of expectations which are tailored to each firm’s circumstances. The exact measures that the PRA may take, according to the degree of integration or independence appropriate for a subsidiary or branch, are described in Chapter 5. The requirements imposed by the ring-fencing regime are in addition to the PRA’s expectations concerning the information and controls required for a firm that is a ring-fenced body to be capable of being adequately supervised as a consequence of its membership of a wider group. Specifically, with respect to branches, where the PRA identifies concerns that a branch would fail to meet the PRA’s expectations for effective supervision, the PRA may exercise its powers under the Financial Services and Markets Act 2000 (FSMA) to apply specific regulatory requirements at the level of the branch on a case-by-case basis. These would principally be intended to ensure there are sufficient financial and operational resources, and appropriate governance at the UK branch level.

- 26/07/2021

Figure 1: PRA expectations for effective supervision

- 26/07/2021

3

General approach, size, and systemic importance

3.1

The PRA has general expectations that underpin its ability to effectively supervise banks and designated investment firms which are part of international groups or headquartered overseas. Subject to these, the PRA’s expectations then vary according to the nature, size, and systemic importance of the UK operations. This, coupled with the degree of information available, effectiveness of co-operation with the home state supervisor, and controls that are in place, influences the degree of separation or integration that is acceptable to the PRA as an operational outcome.

- 26/07/2021

General expectations for effective supervision

3.2

For firms that are part of international groups carrying on banking business in the UK, the PRA first assesses the general factors that must be in place for effective supervision to be possible, and then assesses the factors specific to each international bank and any group of which it is a member.

- 26/07/2021

3.3

The general factors the PRA considers are:

- (a) whether the home jurisdiction’s prudential supervision regime is sufficiently equivalent to the UK regime;

- (b) whether there is sufficient supervisory co-operation with the home state supervisor; and

- (c) the efficacy of the arrangements for resolution. Consistent with the expectations set out in the PRA’s Fundamental Rule 8 and the Bank of England’s (the Bank) Resolvability Assessment Framework where relevant, these arrangements will be assessed in consultation with the Bank as the UK resolution authority.10

Footnotes

- 10. Details available at: https://www.bankofengland.co.uk/paper/2019/the-boes-approach-to-assessing-resolvability.

- 26/07/2021

a) Equivalence

3.4

The PRA assesses the degree to which the home jurisdiction’s prudential supervision regime is equivalent, taking account of the following characteristics of the home state supervisor (this is not an exhaustive list):

- its regulatory framework;

- powers;

- general approach to the supervision of individual firms and the consolidated group;

- information sharing;

- confidentiality; and

- the competence and independence of supervision.

- 26/07/2021

3.5

The PRA will make an overall assessment of whether the home state supervisor is sufficiently equivalent, and whether its regime is consistent with the UK regulatory framework in delivering appropriate outcomes that meet the PRA’s objectives.11 The PRA assesses these factors in their totality, but will place considerable weight on assessing the extent and quality of co-operation with the home state supervisor. The PRA will take into account the supervision of individual firms (including branches) and their consolidated group, and it will consider the nature and scale of a firm’s activities in the UK.

Footnotes

- 11. The PRA’s assessment of equivalence is based on the outcomes achieved and is for the purposes of authorisation and supervision by the PRA, which is separate from advice the PRA may provide to HM Treasury where HM Treasury may make determinations of equivalence for other purposes. The PRA may give advice to HM Treasury pursuant to Regulation 4 of The Equivalence Determinations for Financial Services and Miscellaneous Provisions (Amendment etc.) (EU Exit) Regulations 2019 (SI 2019/541).

- 26/07/2021

3.6

The PRA’s supervisory equivalence assessments are reviewed periodically. The frequency of review is determined by the number, size, and systemic importance of the firms from a home state. The assessments of the home state supervisor focus on the degree to which the home state supervisor’s regime is compliant with the Basel principles in terms of supervisory approach, tools, and practices. In performing the assessments, the PRA will base its analysis on the Basel capital and group supervision standards, the Basel Committee’s Regulatory Consistency Assessment Programme reviews,12; the International Monetary Fund’s Financial Sector Assessment Programme reviews,13 and the Financial Stability Board’s (FSB) peer reviews14 where appropriate, supplemented by other sources as necessary. The PRA will also take account of its own experiences in its interactions with the home state supervisors. It will also be important for the PRA to factor in any conduct concerns that the FCA may raise concerning a jurisdiction.

Footnotes

- 26/07/2021

3.7

Where, in the PRA’s view, a home state supervisor is sufficiently equivalent but there are weaknesses in the way the firm operates, the PRA may propose to add limitations to the nature and scale of activities performed in the UK. In exceptional circumstances, the PRA may not be satisfied that a home jurisdiction delivers equivalent outcomes, but may still authorise a firm to operate as a subsidiary in the UK. However, in those circumstances the PRA will expect the UK subsidiary to operate with a very high degree of independence from the overseas operations, and that the PRA has a high degree of direct supervisory influence on the group in relation to the activities of the subsidiary.

- 26/07/2021

b) Supervisory co-operation

3.8

In considering whether there is sufficient supervisory co-operation with the home and other relevant supervisors, the PRA has the following approach.

- 26/07/2021

3.9

Supervisory co-operation is usually underpinned by the PRA entering into a memorandum of understanding (MoU) with the relevant home state supervisory authority.15 These establish a formal basis for: co-operation, including the exchange of information and investigative assistance; the facilitation of timely and effective supervision; and for the identification of risks to the financial system, including emergency situations.

Footnotes

- 15. The PRA has entered into a new MoU with the European Banking Authority (EBA), and MoUs with other competent authorities in the European Economic Area (EEA), to facilitate continued supervisory co-operation and information sharing. All current MoUs are available here: https://www.bankofengland.co.uk/about/governance-and-funding.

- 26/07/2021

3.10

Footnotes

- 16. August 2003: https://www.bis.org/publ/bcbs100.htm

- 17. June 2014: https://www.bis.org/publ/bcbs287.htm

- 18. September 2012: https://www.bis.org/publ/bcbs230.htm.

- 26/07/2021

3.11

The PRA considers not just whether such arrangements have been agreed, but how well in practice their aims are achieved. The high-level outcomes the PRA expects to see include: transparency over the financial and operational resilience of the group, and the group’s capacity to support the international bank; appropriate equivalence of the home state supervision in practice; and transparency over when and how the home state regulator might intervene to remedy noncompliance with prudential standards along with any triggers for pre-emptive action. To achieve this, the PRA expects there to be regular structured engagement with the home state supervisor, either through a college or bilateral meetings or both, as appropriate, which should facilitate a technical discussion of the material risks and risk management practices at the firm.

- 26/07/2021

3.12

The degree of co-operation with the home state supervisor that the PRA expects is commensurate with the size of the firm, the degree of cross-border integration of its business, and the systemic nature of any wholesale branches operating in the UK.

- 26/07/2021

c) The efficacy of the arrangements for resolution

3.13

This will be a factor in the PRA’s judgements when forming a view on its risk appetite towards subsidiaries and branches operating in the UK. For subsidiaries and branches that perform critical functions in the UK19, the PRA, in consultation with the Bank as UK resolution authority, will assess:

- the credibility or feasibility of the home state supervisor and home resolution authority’s approach to resolvability and resolution execution (including its compliance with the FSB Key Attributes);20

- the ability of the PRA, in consultation with the Bank, to rely on the home state supervisor and home resolution authority to deliver resolvability and if necessary execute the resolution strategy for the group and firm, including the home state supervisor and home resolution authority’s operational capability to implement a resolution and to put in place adequate coordination mechanisms between home and host authorities;

- the adequacy of the group’s and firm’s resolution arrangements:

-

- (i) for the relevant subsidiaries21, taking into account the Bank’s views as to whether the capabilities of the resolution group would deliver resolvability outcomes that are broadly comparable to those set out in the Statement of Policy (SoP) ‘The Bank of England’s Approach to Assessing Resolvability’;22

- (ii) for branches, although the Bank’s Resolvability Assessment Framework (RAF) does not apply to these entities,23 the resolvability outcomes set out in the Bank’s SoP provide relevant context for the Bank’s engagement with the PRA in respect of the authorisation and supervision of the UK branches of overseas banking groups; and

- the willingness of the home resolution authority to share resolution plans with the PRA on request, and to engage in a dialogue with the PRA and the Bank regarding progress on resolvability and the implications of the resolution strategy for any UK subsidiary or branch operating in the UK.

Footnotes

- 19. Critical functions are defined in section 3(1) of the Banking Act 2009. Available at: https://www.legislation.gov.uk/ukpga/2009/1/section/3.

- 20. ‘Key Attributes of Effective Resolution Regimes for Financial Institutions’, October 2014: www.fsb.org/wp-content/uploads/r_141015.pdf.

- 21. July 2019: https://www.bankofengland.co.uk/paper/2020/updates-to-the-boes-approach-to-assessing-resolvability.

- 22. ibid.

- 23. Ibid, paragraph 2.7.

- 26/07/2021

Structural profitability

3.14

The PRA has a minimum expectation that UK subsidiaries of international groups should be on a path to being structurally profitable on a standalone basis (or that the group’s viability depends on supporting the UK operations). That is, they should not be solely cost centres for the group with accumulated costs that are extinguished by periodic capital injections from the group. Rather, the firm should be capable of accreting at least some of its own capital (or contributing to the accretion of group capital), so that operating costs of the international bank are covered on a day-to-day basis by income that it generates. That income may be in the form of service charges to the rest of the group or cross-subsidies built into the pricing and funding arrangements between wholesale and retail business in the firm or other group companies. It is important that the firm and PRA understand the extent of such cross-subsidies in order to assess the soundness of the business. The PRA may request that firms provide evidence that parental support will be provided and the parent has a clear strategy to do so.

- 26/07/2021

3.15

New retail businesses in particular may be loss-making, but as they mature and grow, the PRA expects them to become more profitable and secure. Accordingly, the PRA expects to receive information on the degree of cross-subsidy between the UK retail business and wholesale business within the firm and between the firm and the rest of the group.

- 26/07/2021

3.16

The PRA’s expectation of structural profitability for UK subsidiaries of international groups does not preclude the use of group service companies by firms, whether engaged in retail business or wholesale business, provided operational resilience and operational continuity expectations are met.

- 26/07/2021

Specific considerations for retail business

3.17

The consideration of retail business is of sufficient weight that the PRA considers that good visibility of the risks in the wider group and good supervisory co-operation are not always sufficient to mitigate risks to the PRA’s objectives without separation from the wider group. Chapter 6 of this SS sets out the additional factors that the PRA considers when deciding whether authorisation for a firm to operate a UK branch is appropriate, including certain thresholds above which retail deposits may lead the PRA to conclude that separation of the UK business into a UK subsidiary would be more appropriate (see Chapter 6). Significantly greater amounts of UK retail business may take a firm above the threshold at which it is required to ring-fence its ‘core activities’ under Part IX B of FSMA (as amended).24 This effectively leads to that business being required to have a further degree of separation from the rest of the group.

Footnotes

- 24. £25 billion of ‘core deposits’, as specified in the Financial Services and Markets Act 2000 (Ring-fenced Bodies and Core Activities) Order 2014. Available at: https://www.legislation.gov.uk/ukdsi/2014/9780111117118.

- 26/07/2021

3.18

Where ring-fencing is not required, the PRA does not expect any greater separation to be necessary to mitigate risks to retail business in the UK operations. In general, the degree of separation appropriate will therefore follow the same framework as for wholesale business, as set out below. However, there are three areas which are worth emphasising for firms that are part of international groups regarding their compliance with PRA rules applicable to international banks:

- When branches or subsidiaries outsource to parent or affiliated companies outside the UK, they should ensure that the outsourced service is provided in compliance with UK legal and regulatory requirements, even if these firms are bound by policies, procedures, or written agreements set by their overseas group or parent companies.

- Depositor protection in the UK may be different from that applicable to the overseas group or head office, and so the PRA will pay particular attention to compliance with the Depositor Protection Part of the PRA Rulebook, including the Single Customer View Requirements.

- While the PRA does not require any separation of a firm’s retail business from the rest of the group, or from its wholesale activities, the PRA does expect to receive information on the degree of financial, operational, and other business dependencies (including cross-subsidies) between the UK retail business and wholesale business within the firm, and between the firm and the rest of the group.

- 26/07/2021

Specific considerations for wholesale business

3.19

Wholesale business poses risks to financial stability, particularly when it reaches a scale in the UK that significant losses or operational dependences could cause problems in financial markets or the failure of other financial institutions. The PRA considers size to be a factor when deciding whether to designate investment firms as PRA-regulated firms. The PRA’s approach to this is set out in the SoP ‘Designation of investment firms for prudential supervision by the Prudential Regulation Authority’.25 This SoP sets out the factors that the PRA considers, which include a firm’s total gross assets, or the total gross assets of investment firms in the same group, exceeding £15 billion.

- 26/07/2021

3.20

For international banks with UK branches undertaking wholesale business, in assessing whether the branch is systemically important, the PRA considers (among other things) a similar threshold, where the total gross assets attributed to the branch, and where relevant other UK branches in the group, exceed an average of £15 billion. This is discussed in detail in Chapter 6.

- 26/07/2021

4

Information, co-operation, and controls to be effectively supervised

Firm-specific expectations for effective supervision

4.1

The factors that the PRA considers in assessing its ability to effectively supervise a particular international bank include whether:

- (a) the PRA receives sufficient co-operation, and financial and regulatory information on the overseas risks and financial position connected with the firm, from its group or head office and relevant overseas supervisory authorities (see Box 1);

- (b) any wider group to which the firm belongs has the capacity and willingness to support the firm;

- (c) where the firm’s governance is provided by individuals with roles in a wider group, that governance is effective in taking into account the risks to the firm and, conversely, where the firm’s governance is provided by individuals whose only role is within the firm, those individuals have appropriate influence within the wider group’s management;

- (d) booking arrangements are transparent and effective, and the firm appropriately manages the risks that it originates, receives, and transfers out to affiliates (see Box 2);

- (e) operational resilience arrangements that are in place with other group members are sufficient, in the case of a UK subsidiary, to allow compliance with PRA operational resilience requirements; or, in the case of a UK branch, to assure the PRA that the services the branch offers in the UK are operationally resilient. For branches, the PRA will consider whether the home state’s operational resilience regime is sufficiently robust to deliver outcomes similar to those required by the UK regime, including whether the home state supervisor has adopted the Basel Principles on Operational Resilience and whether the firm can demonstrate that it is in compliance with its home state regime.26 The PRA will also look to gain assurance that operational disruption at group level does not represent undue risk to the group as a whole, and thereby provision of services by the UK business; and

- (f) a credible group resolution strategy, or plans to support or wind up the firm in line with the Bank’s resolution objectives, are in place.

Footnotes

- 26. Basel Committee on Banking Supervision: ‘Principles for Operational Resilience’ (March 2021), at https://www.bis.org/bcbs/publ/d516.htm.

- 26/07/2021

a) Financial and regulatory information, and co-operation

4.2

The PRA expects to have access to certain categories of financial and regulatory information for every international bank in order to be able to assess whether it would meet threshold conditions on authorisation and continue to meet them on an ongoing basis, and to assess the impact that the firm’s activities may have on the stability of the UK financial system. The level of detail will vary according to the size and complexity of the firm’s business. The PRA also expects to receive a broader range of information in situations where the international bank poses a higher risk to financial stability, or where its business is more highly integrated with overseas operations and hence more at risk from activities outside of the PRA’s direct supervision.

- 26/07/2021

4.3

The PRA also follows, and expects other supervisory authorities to follow, the guidance provided by relevant international committees (the Basel Committee on Banking Supervision in particular) concerning supervisory co-operation. In practice, the PRA finds certain aspects particularly conducive to constructive relationships and effective supervision. These matters of what might be regarded as ‘good practice’ are included in Box 1 below under ‘Examples of information that the PRA sees when a strong and co-operative relationship exists with home state supervisors and firms’. These are illustrative rather than a substitute for internationally agreed standards of co-operation.

- 26/07/2021

4.4

Appropriate visibility of group risks is achieved by a combination of an effective co-operative relationship with the home state supervisor and appropriate information sharing by the home state supervisor and the firm. This is particularly relevant at the point of authorisation or where a firm’s circumstances change materially. Where the firm’s scale and operating model require the PRA to have certain information on group risks, the PRA will first discuss the information that it requires with the home state supervisor (with a view to the home state supervisory authority providing this information where possible). The PRA will then discuss appropriate arrangements with the firm concerning any additional information it requires. The PRA, in consultation with the Bank in its capacity as resolution authority, may also require additional information from the home resolution authority and firm regarding the resolution arrangements of firms of such size and complexity that they may pose a higher risk to UK financial stability.

- 26/07/2021

4.5

For each firm that is part of an international group, commensurate with its systemic importance and the degree of cross-border integration of its UK business, the PRA:

- aims to contribute to the supervisory strategy for the group as a whole, and to have insight into the group supervisory strategy, as necessary to achieve the PRA’s objectives;

- expects to agree with the home state supervisor how best to co-ordinate supervisory work where common areas of interest are identified, and to undertake supervisory work in conjunction with the home state supervisor. This could include joint visits to the UK subsidiary or branch in appropriate cases where both the PRA and the home state supervisor have prioritised work in particular areas. It could also include the PRA having direct access to management in the international group or parent where that is relevant to the PRA’s understanding of strategy and risks that may affect the UK operations;

- expects to have a regular and proactive exchange of supervisory assessments with the home state supervisor, such as the results of firm visits or analyses in areas that are of particular relevance to the UK entity;

- expects a prompt exchange of information and proactive notification of issues materially relevant to the UK entity;

- expects to have access to information on governance and financial resilience for the firm as a whole, and the group of which it is part, where it is relevant for the PRA’s supervision of the international bank and the PRA’s objectives; and

- needs to be satisfied, in consultation with the Bank as UK resolution authority, that the resolution authority or authorities in the relevant home jurisdictions for the group have adequate powers and plans for the group’s resolution.

- 26/07/2021

4.6

Box 1 sets out the additional information on group risks, beyond what it receives in respect of the UK business, that the PRA expects to see. In broad terms, the PRA is open to discussion with the home state supervisor and the firm as to how this information is provided. For example, it could be provided through engagement at supervisory colleges, in a structured way as provided to or agreed by relevant supervisory authorities, or in the form of management information prepared by the firm for internal purposes. The PRA also has no specific expectation as to whether information prepared by entities in the group is provided by those entities, the UK entity, or any supervisor, or whether information prepared by supervisors is received directly from supervisors or provided by group entities. Firms and their home state supervisors may decide the process for the provision of information to the PRA based on their individual circumstances. In the case of the smallest firms, the PRA will seek to obtain most of this information from the home state supervisor during its routine supervisory engagement with the PRA and in keeping with arrangements described in an MoU (where this exists between authorities).

- 26/07/2021

4.7

In taking this approach, the PRA aims to minimise the time and effort required to produce the information it needs from supervisory authorities, international banks, or their group entities. The PRA acknowledges that some information, such as supervisory assessments and peer group analyses, can only be provided by supervisory authorities. The PRA expects the information to be refreshed periodically to ensure that it remains relevant over practical timescales and the practical arrangements can be agreed between the home state supervisor, the firm, and the PRA.

- 26/07/2021

4.8

The precise information and data that the PRA will expect to receive may change over time, especially as events and risks crystallise. The PRA will keep its expectations under review and will aim to be proportionate in its requests.

- 26/07/2021

Box 1: The PRA’s expectations for information sharing

The PRA’s expectations for access to information to ensure appropriate visibility of the financial and operational risks of international banks

The PRA needs sufficient information on risks in the group to which the international bank belongs to be satisfied that the threshold condition relating to the PRA’s ability to supervise the firm effectively is met. This information may be provided by the home state supervisor or by the firm.

The information that the PRA expects to have access to will be proportionate, tailored to the firm’s activities and structure, and focused on those group risks which have a direct bearing on the risk profile of the international bank in the context of the PRA’s objectives (eg global trading business lines for which risk is managed or booked to the UK entity). Some information is likely to be provided on a regular basis and some in response to ad hoc requests or particular events.

These will vary according to:

- the firm’s potential impact on the financial stability of the UK economy;

- the degree of interconnection of the UK operations with the overseas part of the firm and group;

- whether the markets in which the firm and group operates are functioning normally or are stressed; and

- any idiosyncratic stresses affecting the firm and its proximity to failure.

The firms and groups in respect of which the PRA would expect to receive the most information are therefore the largest UK subsidiaries and the systemic branches, including those belonging to groups designated as globally systemically important, and those which are most interconnected with the group’s overseas business.

During group or market-wide stress events, the PRA will expect information from the home state supervisor and the firm on the nature, cause, and extent of any idiosyncratic stress, and the frequency and scope of the information shared in some key areas, notably liquidity and profit and loss, will usually need to increase, even for small firms.

Baseline information

The PRA expects, when requested, access to certain categories of information from all international banks, both in times of crisis and normal business, namely proportionate and timely information on:

- the nature of the firm’s and group’s business model, and any material changes in it, to the extent that they could have a material impact upon the firm or the group’s ability or willingness to support it.

- the financial resilience of the firm and the firm’s immediate (and ultimate, if different) overseas parent, or the consolidated international financial group to which the firm belongs. Information on financial resilience includes capital and liquidity positions relative to relevant regulatory requirements;

- the operational resilience of the firm and group, including risks arising elsewhere in the group that may affect the ability of the firm to deliver its important business services or critical operations (such as those provided through intragroup outsourcing or other inter-affiliate arrangements);27

- material risks to the firm’s survival emanating from any group to which it belongs, including enforcement or legal actions;

- the group’s recovery plan, including details regarding financial and non-financial dependencies between group entities, consistency of recovery operations, and the impact of group recovery options on the UK firm; and

- resolution planning, including information regarding the group’s preparations for resolution consistent with Fundamental Rule 8 (the PRA, and the Bank as resolution authority, will discuss with one or both among the home state supervisor and home resolution authority, and then consider if any additional information is required from the firm).

Under normal market conditions, the PRA will usually expect to receive more than this baseline of information only for those international banks that have the potential to cause some disruption to the UK financial system. For the smallest firms, the PRA will seek to obtain most of this information from the firm’s home state supervisor during its routine supervisory engagement with the PRA and in keeping with arrangements described in any relevant MoU.

Additional information expected for highly integrated or systemically significant businesses

The PRA expects to receive additional information in situations where a firm’s business model or operations are highly integrated with its group’s overseas business and where it is significant systemically.

Firms typically run their investment banking and trading activities on a global basis, with complex booking arrangements (see also Box 2). The PRA needs to understand the portion of global risk that is managed in the UK, what UK risk is managed elsewhere, and how the UK business performance sits within the overall performance of the firm and group. For trading activities, timely information on business line performance is a critical indicator of emerging market and firm-specific risks.

For highly integrated firms that rely on global systems, including custodians, the PRA may expect additional information relating to group operational resilience and the performance of group IT systems.

Examples of information that the PRA sees when a strong and co-operative relationship exists with home state supervisors and firms

For the largest firms with the most potential impact on UK financial stability, the PRA will first discuss with the home state supervisor what information the PRA requires and what might be provided by the home state supervisor. The PRA will then discuss appropriate arrangements with the firm concerning any additional information required. Illustrative examples of such information include:

- the provision by the firm of daily or weekly profit and loss figures covering global and local investment banking and trading business lines;

- information on the firm’s structural profitability and any material element of cross-subsidy between business lines;

- weekly or monthly group market risk reports;

- provision by the home state supervisory authorities of the outputs from reviews, for example, the Supervisory Review and Evaluation Processes;

- provision by the home state supervisory authorities and the firms of information on their stress tests and how these affect the UK branch or subsidiary;28

- provision by one or both of the home state supervisory authorities and the relevant firms of group liquidity information, regularly in business-as-usual periods and more frequently once there is agreement that we have entered a period of market stress;

- any material change in the operational resilience of the firm or group, for example cyber-attacks, that may affect the group systems that are used by the UK business or which threaten the survival of the firm or group;

- material findings from internal risk or audit functions, or external audit reviews (particularly where there are common group wide systems and controls);

- information on the home state and group approach to climate risks, where these may help the PRA to understand the group risk profile and how this may affect operations in the UK; and

- from the home resolution authority or through crisis management groups, and the group’s resolution planning information, including the group’s plans and capability to wind down trading activities in an orderly and solvent fashion insofar as these affect UK operations.

Footnotes

- 27. Important business services refers to services as defined in the Operational Continuity Part of the PRA Rulebook which applies to CRR firms – ie UK subsidiaries of international groups. Critical operations refers to services as defined in the Basel Committee on Banking Supervision’s ‘Principles for Operational Resilience’ (March 2021), found at https://www.bis.org/bcbs/publ/d516.pdf, and is relevant for UK branches.

- 28. UK investment banking subsidiaries of foreign owned banks are currently outside the UK system wide stress testing framework on the basis that the relevant results of home state testing are shared. See Box 5 of the ‘The Bank of England’s approach to stress testing’, October 2015, available at: https://www.bankofengland.co.uk/-/media/boe/files/stress-testing/2015/the-boes-approach-to-stress-testing-the-uk-banking-system.

- 26/07/2021

b) Capacity and willingness to support the international bank

4.9

As regards the group’s capacity and willingness to support a subsidiary, the PRA expects UK subsidiaries to be financially resilient on a standalone basis. But beyond this, there are situations where the ability of the group to support other group entities, including the UK operations, needs to be taken into account. These are, for example, where assessments need to be made of the diversification of risks within the group and of the extent to which funding through debt at the parent level is used to support equity at a subsidiary level, increasing reliance on distributions from equity to service such debt. It is also a consideration when assessing intragroup large exposures and whether parental support to entities in the wider group mitigates the risk that amounts owed to UK subsidiaries will not be repaid. The PRA also has expectations concerning information on the firm’s operational resilience where this depends on group systems (see paragraph 4.26).

- 26/07/2021

4.10

There may be some situations where explicit guarantees of international banks are expected from another group entity, for example with respect to an international bank’s ability to access central bank funding.

- 26/07/2021

4.11

The PRA will establish a view, at least at a minimum in qualitative terms, on the capacity and willingness of the group to support subsidiaries in stressed scenarios, and any barriers to that support arising from the regulatory regimes that apply to it.

- 26/07/2021

4.12

The Bank already takes a similar approach when setting internal minimum requirements for own funds and eligible liabilities (MREL) for hosted subsidiaries. As set out in the Bank’s SoP ‘The Bank of England’s approach to setting a minimum requirement for own funds and eligible liabilities, in deciding whether to set internal MREL for a material sub-group or subsidiary above 75% scaling, the Bank will take into account the resolution strategy applicable to the group and the credibility of the resolution plan for delivering it, and the availability of other uncommitted resources within the group that could be readily deployed to support the material subsidiary, among other factors.29

Footnotes

- 26/07/2021

c) Governance and risk management

4.13

The PRA recognises the fiduciary duties of directors of subsidiaries. Subsidiary boards must also be capable of acting in the best interests of the firm for which they are responsible, as well as safeguarding its safety and soundness.30

Footnotes

- 30. Section 12, SS5/16 ‘Corporate governance: Board responsibilities’, March 2016: https://www.bankofengland.co.uk/prudential-regulation/publication/2016/corporate-governance-board-responsibilities-ss.

- 26/07/2021

4.14

The principles of good governance should apply to all PRA-regulated subsidiaries, including the principle that boards should have sufficient independence, to help ensure they can provide effective challenge to the business. Where a smaller and less complex subsidiary proposes not to have an independent non-executive chair, the firm should still be able to explain how its governance arrangements will otherwise satisfy the need for independent oversight of the executives. Moreover, all firms have an obligation to ensure that all their directors, in particular non-executives, act with sufficient independence of mind and ‘make their own sound, objective and independent decisions and judgments when performing their functions and responsibilities’.31 The non-executive directors on the board should hold management to account against the matters delegated, and be able to challenge the executive effectively and promptly. Firms should have regard to the expectations on board responsibilities outlined in SS5/16 ‘Corporate governance: Board responsibilities’.32

Footnotes

- 31. Joint European Securities and Markets Authority (ESMA) and EBA Guidelines on the assessment of the suitability of members of the management body, paragraph 80. Available at: https://eba.europa.eu/regulation-and-policy/internal-governance/joint-esma-andeba-guidelines-on-the-assessment-of-the-suitability-of-members-of-the-management-body. See also the General Organisational Requirements Part of the PRA Rulebook.

- 32. March 2016: https://www.bankofengland.co.uk/prudential-regulation/publication/2016/corporate-governance-board-responsibilities-ss.

- 26/07/2021

4.15

The UK subsidiary or branch should establish, implement, and maintain adequate risk management policies and procedures, including effective procedures for risk assessment, which identify the risks relating to its activities, processes, and systems, and where appropriate, set its risk appetite or the level of risk tolerated.33 As noted in the PRA’s approach to banking supervision, senior management should embed the principle of safety and soundness in the culture of their organisation.34

Footnotes

- 33. SS4/16 ‘Internal governance of third country branches’, February 2016: https://www.bankofengland.co.uk/prudential-regulation/publication/2016/internal-governance-of-third-country-branches-ss.

- 34. Paragraph 42, October 2018: https://www.bankofengland.co.uk/prudential-regulation/publication/pras-approach-to-supervision-of-the-banking-and-insurance-sectors.

- 26/07/2021

4.16

Where group risk management decisions are being taken which could have an effect on the UK subsidiary or branch, those decisions should take into account the views of representatives from the subsidiary or branch. Those representatives should be given sufficient access to, and influence in, the relevant decision-making committee(s). Firms should take into account their size and internal organisation and the nature, scale, and complexity of their activities when developing and implementing policies and procedures.35

Footnotes

- 35. EBA ‘Guidelines on internal governance under Directive 2013/36/EU’, paragraph 18. Available at: https://eba.europa.eu/sites/default/documents/files/documents/10180/1972987/eb859955-614a-4afb-bdcd-aaa664994889/Final%20Guidelines%20on%20Internal%20Governance%20(EBA-GL-2017-11).pdf

- 26/07/2021

4.17

To meet the PRA’s expectations on information sharing, it is desirable to ensure appropriate connectivity between the firm and its head office or with the parent company board. For example, in the case of a UK subsidiary, a non-executive director from the group board may sit on the local board (or vice versa), or the local chairs of the Risk and Audit Committees may meet regularly with their counterparts at the parent.

- 26/07/2021

4.18

Where the group has a large-scale operation comprising both a branch and subsidiary in the UK, and together they are systemically important, then even though the PRA generally expects branches and subsidiaries to have independent governance arrangements (to safeguard against conflicts of interest in how risks are booked into the UK), the need for there to be a holistic view of UK risks may be more important. In those circumstances, it may be appropriate to have either a UK or regional Chief Executive Officer (CEO) overseeing the whole UK footprint, and potentially other arrangements to ensure it has a comprehensive view of the risks the firm runs in the UK.36

Footnotes

- 36. This includes consideration of group risks; see for example the Risk Control and Group Risk Systems Parts of the PRA Rulebook.

- 26/07/2021

Accountability of Senior Management Functions (SMFs)

4.19

A subsidiary should ensure that they have an appropriate number of SMFs according to its size, complexity, and governance structure, in line with the principles outlined in SS28/15 ‘Strengthening individual accountability in banking’.37 Firms should particularly ensure that Management Responsibilities Maps and Statements of Responsibilities (SoR) are up to date and that responsibilities are allocated in accordance with the Allocation of Responsibilities Part of the PRA Rulebook and SS28/15.38

Footnotes

- 37. July 2015: https://www.bankofengland.co.uk/prudential-regulation/publication/2015/strengthening-individual-accountability-in-banking-ss.

- 38. Statements of Responsibilities are those required by section 60 (2A) of FSMA. Available at: https://www.legislation.gov.uk/ukpga/2000/8/section/60

- 26/07/2021

4.20

Where applicable, the PRA expects firms to allocate the responsibility for overseeing the firm’s booking arrangements to an SMF, and record this appropriately in their Statement of Responsibilities. Where individuals in the parent or in group entities exercise significant influence over the management or conduct of one or more aspects of the firm’s UK regulated activities, it may be appropriate for them to be approved as a Group Entity Senior Manager (SMF7). However, firms have applied for individuals performing a range of functions to be approved as SMF7. Examples include:

- group executives on the board of a UK subsidiary (including smaller firms where parent executives may sit on a UK subsidiary board as non-executives);

- global business line heads operating as senior executives at a UK branch or subsidiary; and

- individuals who combine a global or group role with key responsibilities in the UK (and with significant influence over the UK branch or subsidiary), such as global heads of technology, heads of internal audit, and global heads of operations.

- 26/07/2021

4.21

However, while these examples may be helpful, ultimately whether an individual requires approval as a SMF7 is assessed by the PRA on a case-by-case basis.

- 26/07/2021

4.22

In the case of a firm that has a UK systemic wholesale branch which is part of a group based overseas, and an individual in a related group entity has significant influence over the branch’s booking arrangements, that individual should seek approval as SMF7 (see Box 3).

- 26/07/2021

4.23

Where applicable, the PRA expects firms to allocate the responsibility for overseeing the firm’s booking arrangements to an SMF, and to record this appropriately in their SoR.

- 26/07/2021

d) Booking arrangements

4.24

The PRA is open to firms operating a diverse range of booking arrangements, including globally integrated structures, provided that they meet the PRA’s expectations as set out in Box 2.

- 26/07/2021

4.25

By booking arrangements, the PRA means the front-to-back lifecycle of trading, from origination, trade execution, risk capture and transfer, through to back-office settlement. The PRA seeks to ensure that firms have appropriate controls for the full lifecycle of their trades. At the start of the lifecycle, a firm should include within its control framework those traders managing the risk directly and those facilitating the execution and delivery of risk to the firm’s balance sheet, such as sales people or sales traders. In terms of activity, the PRA’s expectations in Box 2 relate primarily to the trading book. However, the PRA recognises that some of items housed in the banking book will pose similar risks given their nature, and firms should consider whether and how their booking frameworks and controls should be extended to cover them.

- 26/07/2021

Box 2: The PRA's expectations for booking arrangements

Booking arrangements should be transparent and the firm should appropriately manage the trading risks that it originates, receives, and transfers out to affiliates.

Transparency

For those international firms with large-scale trading businesses, characterised by global risk management hubs, it is essential that the risks in the relevant global business, and how this affects the risk profile of UK operations, are visible to the PRA and that the PRA and home state supervisor have the same understanding of those risks. With a global business line, risks may crystallise anywhere in the group. Given the UK’s role as a global centre for trading, those risks are often observed first in the UK. Therefore, if the firm is to operate a fully integrated global business model, the PRA needs to understand the risk profile of an entity in the context of the global business lines of which that entity is a part.

The PRA has a number of expectations concerning how the local entity should organise its booking arrangements in order that it meets the threshold conditions on the prudent conduct of business and its obligations under Fundamental Rules 3, 5, 6, and 8, relating to risk management and resolvability.

Management and controls: The PRA’s expectations

1. Firms should set out a clear rationale for their booking arrangements, document the booking arrangements, and have them approved by the appropriate governance body.

Firms should have a policy document that sets out a clear rationale for their UK booking arrangements, and how those arrangements align with the business model for its UK authorised business. The firm’s arrangements should be part of a coherent strategy for the group and firm. The policies should be drafted with sufficient coverage and detail, such that the role of the international bank within the group’s global booking arrangements is clear.

This document should be approved by the relevant governance body in the UK. For example, this may be the board for a subsidiary or the executive management committee for a branch.

2. Firms should have adequate systems and controls in place to ensure that intended booking arrangements are followed in practice.

The PRA’s rules require firms to have comprehensive and proportionate controls and to review their adequacy regularly.39 The PRA has certain expectations as to how these booking arrangements should be controlled.

Firms should regularly assess the risks that they face due to the booking model choices they apply, rate them as for any other risk, and consider effective mitigations, including the need for new or modified controls. These controls should ensure that the intended booking arrangements are followed — ie a firm’s booking policy should always be translated into appropriately enforced controls through its control framework to avoid ambiguity. This control framework should also be approved by the relevant governance body in the UK, as outlined in point 1 above.

For example, an international bank with a material trading business should have a mix of detective and preventative trading controls — ie pre-trade (soft and hard block) checks and post-trade checks.

- Remote bookers (traders in non-UK entities booking onto a UK entity) should be subject to appropriate controls and formal oversight, including an appropriate risk assessment. Where the UK entity allows material remote booking onto its books, but the trader is not subject to direct trader oversight by the UK entity (often called ‘orphan books’), it may be appropriate to assign shared coverage of this remote book to a UK-based trader or to UK-based risk management staff. This includes risks that may arise at all stages of the trade life-cycle, including back-office settlement.

- Where a firm relies on back-to-back booking extensively, a higher degree of assurance should be obtained through the use of automated trade mirroring, reconciliation, and monitoring processes.

- Management information related to trades undertaken or booked in the UK, booking risks, and compliance monitoring should be timely and comprehensive, disaggregating the relationship between the UK entities and those of affiliates and providing measures of change. It should distinguish between remote booking into and out of the UK entities. The management information should be routinely shared with the appropriate committees, and any breaches of the policy should be subject to appropriate sanctions.

Any deviations from the booking model policy should occur rarely and only by way of an explicitly approved exception process documented in the same policy with appropriate involvement of the UK entity.

These procedures are expected to be subject to internal audit assessment.

For an international group, the location of the resulting risks should be transparent to each legal entity. This requires an ability for the reporting of such risks to be readily disaggregated by entity.

3. Firms with major trading activities should ensure that responsibility for ensuring that there are appropriate controls in place to manage its booking arrangements, including remote booking, is allocated to a senior management function.

The responsibilities for ensuring that the firm’s booking arrangements are appropriately controlled and monitored should be explicitly set out in the statement of responsibilities for the responsible senior management functions.

4. The international bank should have an appropriate local risk management capability.

While a firm may rely extensively on its group for booking, risk management, and other services, the PRA considers that the firm should have sufficient risk management capabilities if it is to satisfy the relevant threshold conditions and comply with the Fundamental Rules. In particular, it will need adequate financial and non-financial resources, including a sufficient number of qualified staff dedicated to the management and control of the UK branch or subsidiary. The risk management capabilities should be explicitly considered and sized appropriately during the approval of the UK booking model policy and the controls required, as described above.

The need for sufficient local risk management capabilities is primarily to support the entity’s effective supervision of UK-based traders, but also aims to manage the risks to the UK entities arising from the global booking model. For example, the UK branch or subsidiary may hold risk that has been transferred to the UK from elsewhere in the group, rather than risk originated from UK client business.

Where there is risk transfer onto the firm’s balance sheet, through remote or back-to-back booking from an affiliate, there should be appropriate controls around that process. If those risks are analogous to risks arising from dealings with external third parties, then they should be subject to commensurate controls, as would be appropriate for direct dealings with external third parties. Staff in the UK entity should have accountability for managing such risks.

Firms will also need sufficient local risk management capabilities if their booking structures, exposures, and associated risk management are to be resilient in the event of interruption to the flow of group services.

Having a portion of group risk managed in the UK is likely to facilitate an orderly group and local resolution. The more important the international bank is to the wider group, the more likely it is that its survival is essential to the group’s resolution.

5. There should be a broad alignment of risk and returns at the entity level.

Subsidiaries should not be designed to be structurally-loss-making, but should aim to be solvent and viable.

Firms operating in the UK may act as service providers to their groups, but they should be appropriately remunerated for those services.

6. The firm’s booking arrangements should not be an impediment to the firm’s recovery and resolution or to any plan to wind down trading in a solvent and orderly fashion.

While a global booking model may not be considered a direct impediment under a single point of entry resolution strategy, it could add complexity to the restructuring of the group post resolution. Under a multiple-point-of-entry (MPE) strategy, the inter-connectivity between the UK entity and the group associated to a global booking could be an impediment to resolution that the firm should address.40 Similarly, where contingency plans to be able to wind down trading books in a solvent and orderly fashion are important to any orderly exit, recovery, or resolution strategy, the PRA expects that the particular booking model adopted by a firm will have been fully taken into account in those plans.

Footnotes

- 39. Including Fundamental Rules, General Organisational Requirements 2.1–2.2, Compliance and Internal Audit 2.1, Internal Governance of Third-Country Branches 2, 6, and 8, and Risk Control.

- 40. MPE refers to a resolution strategy that envisages applying resolution powers to multiple entities within a group. See ‘The Bank of England’s approach to resolution’, October 2017: https://www.bankofengland.co.uk/paper/2017/the-bank-of-england-approach-to-resolution .

- 26/07/2021

e) Operational resilience

4.26

The PRA expects international banks to understand the services they provide to external end users in the UK, and the risk posed to the firm’s safety and soundness in the event of a severe but plausible disruption to such services.41 The PRA expects that firms should be prepared to identify these services to the PRA, and articulate the point at which disruption to these services poses a risk to the firm’s safety and soundness or the financial stability of the UK (if appropriate).

Footnotes

- 41. The relevant services are, in the case of UK subsidiaries, the ‘important business services’ as defined in the Operational Continuity Part of the PRA Rulebook, and in the case of UK branches, the PRA will, in the first instance, look to the ‘critical operations’ a firm may have identified, as defined in the Basel Committee on Banking Supervision’s ‘Principles for Operational Resilience’ (March 2021), available at https://www.bis.org/bcbs/publ/d516.pdf.

- 26/07/2021

4.27

The PRA considers international banks should have a sufficient understanding of the necessary operational resources that are used to deliver such services, regardless of geographic location, in order to adequately understand the risk posed to the firm’s safety and soundness or the financial stability of the UK in the event of severe but plausible operational disruptions.

- 26/07/2021

4.28

In addition, the PRA will consider the robustness of the home state’s operational resilience regime, to gain assurance that operational disruption at the group level does not represent undue risk to the group as a whole, and thereby provision of services by the UK business. This will be particularly relevant where functions are outsourced by the international bank to other parts of its group, and for branches, as they are not subject to the PRA’s rules on operational resilience.

- 26/07/2021

f) Group-specific resolution strategy

4.29

The PRA works with the Bank as UK resolution authority to ensure that where a firm fails, it does so in a way that avoids significant disruption to the supply of critical functions to its customers and other counterparties. It is the Bank’s responsibility to set the resolution strategy, set MREL, and ultimately execute any resolution, but the PRA acts in co-operation with the Bank to ensure that firms have appropriate resolution arrangements in place as part of going concern supervision, consistent with Fundamental Rule 8. Consequently, resolvability is an important consideration in the PRA’s supervisory approach to international banks. The effectiveness of the home state regime and the credibility of a group’s resolution strategy, and the resolvability outcomes set out in the Bank’s RAF, where relevant, are an integral part of the assessment.

- 26/07/2021

4.30

The PRA will consider in particular:

- the alignment of the firm’s group resolution strategy set by the home resolution authority with the PRA’s objectives, including whether it ensures the continuity of the firm’s critical functions in the UK;

- the credibility and feasibility of the firm’s group resolution strategy, including a clear process to identify and remove barriers to resolution by the home state supervisor or home resolution authority involving the host authorities, including the PRA; and

- the adequacy of the firm’s resolution arrangements, consistent with Fundamental Rule 8 and the RAF:

- for the relevant subsidiaries, the PRA will take into account the Bank’s assessments as to whether the capabilities of the group would deliver resolvability outcomes that are broadly comparable to those set out in the Bank’s SoP ‘The Bank of England’s Approach to Assessing Resolvability’;42 and

- for branches, although the RAF does not apply to these entities, the resolvability outcomes set out in the Bank’s SoP provide relevant context for the Bank’s engagement with the PRA in respect of the authorisation and supervision of the UK branches of overseas banking groups.43

Footnotes

- 42. July 2019: https://www.bankofengland.co.uk/paper/2019/the-boes-approach-to-assessing-resolvability.

- 43. Ibid, paragraph 2.7.

- 26/07/2021

5

Integration and independence

5.1

Once the PRA has considered the effectiveness of supervision that it is possible to exercise given the understanding it has of risks in the wider group, including the level of co-operation and information it is receiving and the controls in place, as well as the size and systemic importance of the international bank, it will consider whether the degree of operational integration or separation is commensurate with those factors. The aspects of integration considered are:

- (a) governance;

- (b) capital and liquidity;

- (c) booking risk management;

- (d) operational resilience;

- (e) resolution strategy; and

- (f) structural profitability.

- 26/07/2021

5.2

There is no automatic or fixed outcome that the PRA applies in terms of the degree of integration or separation that is appropriate, but the PRA applies a graduated set of expectations which are tailored to each firm’s circumstances (see also Chapter 6). The better expectations on effective supervision are met, the more the PRA is content for a business in the UK to be highly integrated with the wider foreign group, or with the foreign operations of the firm if it is operating through a branch.

- 26/07/2021

5.3

Where the information or co-operation the PRA receives are such that the PRA’s expectations for effective supervision are not fully met given the degree of operational integration that an international bank currently has, then the PRA will consider taking measures to require the UK operations of the international bank to be more independent.

- 26/07/2021

a) Governance

5.4

The PRA is likely to expect that there is a greater degree of independence of the governance committees of an international bank subsidiary when the PRA has limited information on how much influence is being exerted by group management, when the degree of influence that UK management has on the group’s strategy is inadequate, or when management of the UK entity is dominated by group strategy. This could be in the form of the proportion of independent nonexecutive directors on the board of the international bank, for instance.

- 26/07/2021

5.5

As set out in SS5/16, the PRA also considers it generally undesirable for some key positions on the board of a subsidiary, such as chair, chair of the key board sub-committees, chief executive, or finance director, to be occupied by executive members of the group or parent board. In circumstances where these appointments may be permissible, such as for certain smaller less complex firms, the firm should be able to explain how its governance arrangements will otherwise satisfy the need for independent oversight of the executives.

- 26/07/2021

5.6

Where the PRA has concerns about the effectiveness of supervision over UK branches owing to their relationship with their head office, other UK branches, or UK subsidiaries, or any wider group, additional governance requirements may be considered. For example, to ensure appropriate governance at the UK branch level, the PRA may require the firm to apply for additional SMFs (such as Chief Risk Officer (CRO), Chief Finance Officer (CFO), Chief Operating Officer (COO), or a group executive under SMF7), or to create a local management committee (or equivalent) for the branch.

- 26/07/2021

b) Capital and liquidity requirements

Capital

5.7

The PRA’s assessment of the PRA buffer will take into account the extent to which wider group risks are visible to the PRA, taking into consideration the systemic importance and the degree of integration of the international bank. Capital is not set at UK branch level.

- 26/07/2021

5.8

As explained in the SoP ‘The PRA’s methodologies for setting Pillar 2 capital’, where the PRA assesses a firm’s risk management and governance to be significantly weak, it may also set the PRA buffer to cover the risks posed by those weaknesses until they are addressed.44 This will generally be calibrated in the form of a scalar applied to the amount of Common Equity Tier 1 (CET1) capital required to meet the Total Capital Requirements (TCR). The scalar could be up to 40% of the total CET1 TCR.

- 26/07/2021

5.9

A firm’s exposures to entities in its own group are generally treated as exposures to a third party and are subject to large exposure limits. Firms can however apply to the PRA for a non-core large exposures group permission, which allows firms to apply a higher large exposure limit to certain entities within their group provided these entities meet certain conditions.45

Footnotes

- 45. SS16/13 ‘Large Exposures’, June 2018: https://www.bankofengland.co.uk/prudential-regulation/publication/2013/large-exposures-ss.

- 26/07/2021

5.10

These permissions increase connectivity with the wider group and increase the contagion risk to the UK entity. For this reason, the PRA will still make a wider judgement whether it is appropriate to grant these permissions, even where the conditions are met. The PRA will consider whether group entities are strongly incentivised to support each other, and whether the treatment is consistent with the overall business model of the firm and furthers the PRA’s safety and soundness objective.46

Footnotes

- 46. See paragraph 3.9 of SS16/13.

- 26/07/2021

Liquidity

5.11

In deciding what liquidity guidance to give a firm under Pillar 2, the PRA will consider how integrated the UK business is with that of the wider group, and the quality of its relationship and the information exchange with the home state supervisor.47

Footnotes

- 47. See SoP ‘Pillar 2 liquidity’, October 2018: https://www.bankofengland.co.uk/prudential-regulation/publication/2018/pillar-2-liquidity.

- 26/07/2021

5.12

The liquidity guidance may be flexed by adjusting the Pillar 2 liquidity add-ons, applying different preferential treatments of intragroup liquidity flows in the Liquidity Coverage Requirement, or by using committed facilities from parent entities.

- 26/07/2021

5.13

Where the PRA has concerns about the liquidity position of the firm or the effectiveness of supervision over branches, the PRA may set additional branch liquidity requirements to ensure appropriate liquidity at the UK branch level, for example by requiring the holding of additional liquidity to ensure sufficient resources are held locally to allow time to respond to a stress at the branch.

- 26/07/2021

c) Booking risk management

5.14

The PRA has a number of high-level expectations of how firms should manage their booking arrangements for trading activity, as set out in Box 2. These are aimed at ensuring that a firm’s booking arrangements are transparent and well-controlled.

- 26/07/2021

5.15

The PRA is open in principle to a wide range of booking models. It recognises that trading activity is often run as a global business model. The UK entity may rely extensively on its affiliates for business origination and for risk management services, but the UK entity remains responsible for ensuring that the level of risk management is appropriate to the risks undertaken.

- 26/07/2021

5.16

Where a firm meets the PRA’s expectations for booking models, the PRA is open to hosting highly integrated and large-scale trading operations.

Where a firm is not able to meet these expectations, the PRA may require more local risk management or limit the degree of connectivity that the firm has with the rest of the group so that less risk is brought into or transferred out of the entity. The PRA may consider a firm unable to meet these expectations if:

- its controls are not commensurate to the risks posed by a complex booking arrangement;

- there is inadequate visibility of the group risk profile, inadequate information sharing, or inadequate home state co-operation; or

- booking arrangements would impede the execution of the resolution plan.

- 26/07/2021

d) Operational resilience

5.17

The PRA expects firms to observe high standards in the management of operational as well as financial risks. If the PRA does not have sufficient understanding of how operational resilience is assured when an international bank is dependent on group or overseas systems and policies, then the PRA would expect those systems or policies to be improved and made clear to the PRA, or for the international bank to become less dependent on those systems.

- 26/07/2021

e) Resolution strategy

5.18